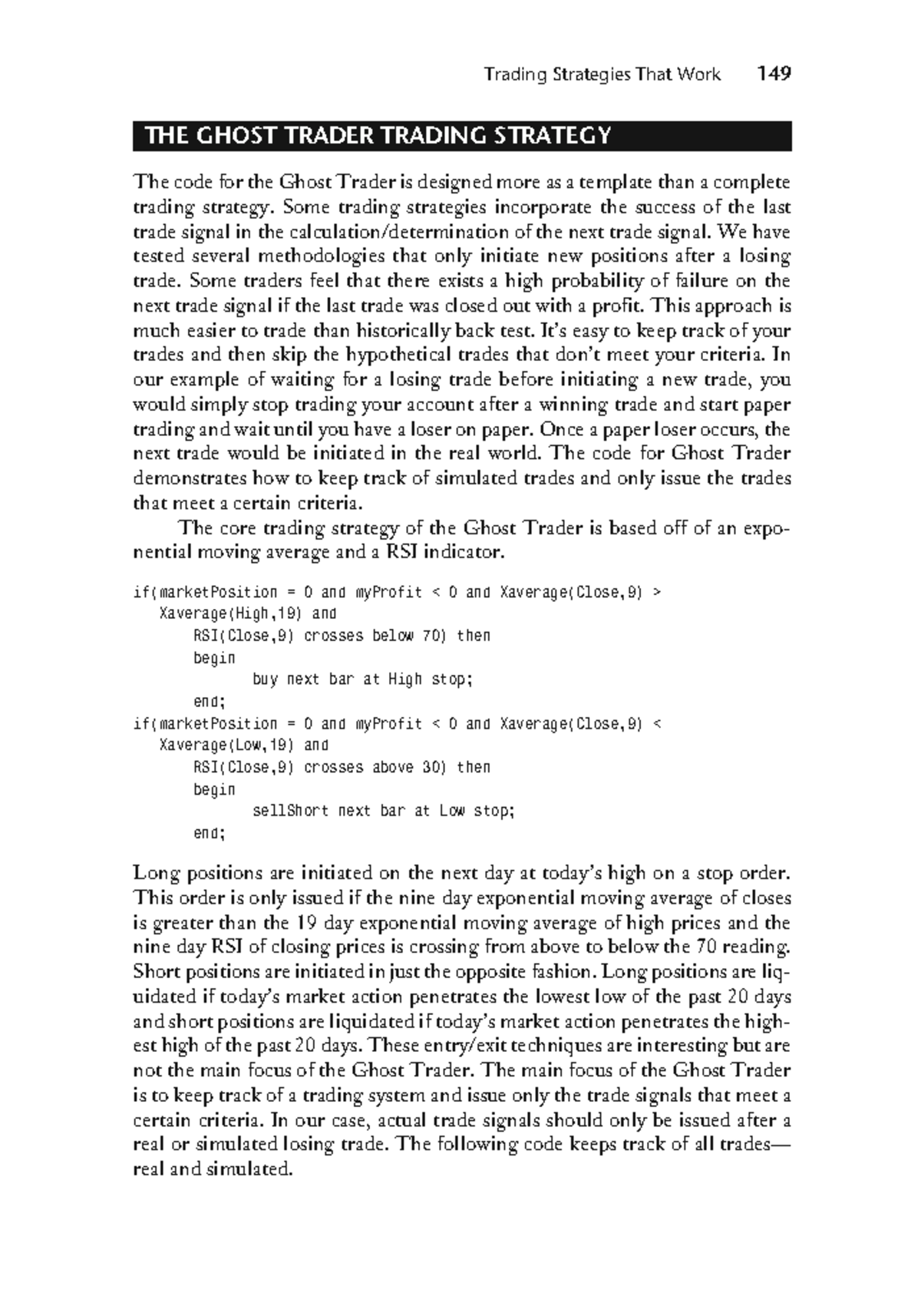

The era of the "free lunch" in Asian capital markets has officially expired. For decades, the Bank of Japan (BoJ) served as the world’s most reliable pawn shop, offering near-zero interest rates that allowed investors to borrow yen cheaply and dump that capital into higher-yielding assets across Southeast Asia and beyond. This "carry trade" wasn't just a financial quirk; it was the structural foundation of the region's growth. Now, as the BoJ finally steps away from its negative interest rate policy and begins the slow crawl toward normalization, that foundation is cracking. The shift is forcing a total overhaul of how East Asian nations fund their infrastructure, manage their debt, and protect their currencies.

The Great Yen Rebound

When Japan moved its short-term interest rates into positive territory, it sent a tremor through the bond markets that many saw coming but few were prepared to handle. The math is simple but brutal. For years, the yen was the ultimate funding currency. You borrowed yen at 0.1%, swapped it for Thai baht or Indonesian rupiah, and pocketed the difference. This constant selling pressure kept the yen weak and the regional investment pump primed.

Now, that flow is reversing. As Japanese yields rise, domestic institutional investors—the massive insurance firms and pension funds—are bringing their money home. Why take the risk of emerging market volatility when you can get a respectable, safe return in Tokyo? This repatriation of capital is draining liquidity from regional bond markets, driving up borrowing costs for everyone from Manila to Hanoi.

The Dollar Trap and the Search for a Third Way

For most of East Asia, the alternative to yen-denominated debt has always been the U.S. dollar. But relying on the dollar is a dangerous game. When the Federal Reserve keeps rates high to combat inflation, and the BoJ stops subsidizing the global money supply, emerging economies find themselves in a pincer movement. Their local currencies devalue against a surging dollar, making their existing dollar-denominated debt significantly more expensive to service.

We are seeing a desperate scramble for "financial autonomy." Countries are no longer content to be pawns in the tug-of-war between the Fed and the BoJ. This has led to an aggressive push for local currency bond markets. The logic is sound: if you can borrow in your own currency, you eliminate the exchange rate risk that has historically bankrupted developing nations. However, building a deep, liquid bond market from scratch is a decades-long project, not a quick fix for a sudden liquidity crunch.

Why Corporate Debt is the Real Red Zone

While much of the media focus remains on sovereign debt, the real danger lurks in the corporate sector. Many of East Asia’s largest conglomerates—the engines of regional GDP—have balance sheets heavily exposed to yen and dollar fluctuations.

During the years of Japanese monetary easing, these firms loaded up on cheap debt to fund aggressive expansions. They didn't just build factories; they bought competitors and ventured into speculative real estate. Now, they face a "refinancing wall." As their old, cheap debt matures, they must replace it with new loans at significantly higher interest rates.

"The risk isn't just a slowdown in growth; it's a series of high-profile defaults that could trigger a systemic banking crisis in the region."

This isn't a hypothetical threat. We are already seeing credit spreads widen for mid-tier developers and industrial firms across the ASEAN bloc. When the cost of capital doubles in a twenty-four-month window, the business models of many "zombie firms" simply cease to function.

The Rise of the Samurai Bond

Paradoxically, as the BoJ raises rates, the "Samurai bond" market—where foreign entities issue yen-denominated bonds in Tokyo—is seeing a strange surge in interest. Why would you issue debt in a currency that is getting more expensive?

The answer lies in relative costs. Even with the BoJ’s hikes, Japanese rates remain significantly lower than those in the United States or Europe. For a sovereign issuer in South Korea or a large state-owned enterprise in Indonesia, issuing a Samurai bond is still "cheaper" than hitting the dollar market, provided they can hedge the currency risk.

But this is a sophisticated game. It requires complex derivatives and a stable outlook on the yen’s terminal rate. It is no longer a trade for the faint of heart or the poorly capitalized. It is a professional’s market, and the amateur hour of the 2010s is over.

The Geopolitical Pivot

Money never moves in a vacuum. The shift in Japan’s financing model is happening alongside a massive geopolitical realignment. China’s slowing economy and its own internal debt struggles mean that Beijing is no longer the "lender of last resort" it once was for its neighbors.

Japan, despite its domestic struggles, is using its financial muscle to offer an alternative to China’s Belt and Road Initiative. By recalibrating its bond market and offering more structured bilateral financing, Tokyo is positioning itself as the "responsible" adult in the room. This isn't just about interest rates; it's about who owns the plumbing of Asian trade and infrastructure for the next fifty years.

The Mathematical Reality of $Yen$ Normalization

To understand the scale, consider the sheer volume of Japanese overseas investment. Japanese investors hold trillions in foreign assets. Even a small percentage shift in their allocation—moving just 5% of their portfolios back into JGBs (Japanese Government Bonds)—represents a massive withdrawal of liquidity from global markets.

$$\Delta L = \sum_{i=1}^{n} (A_i \cdot \Delta w_i)$$

Where $\Delta L$ is the change in global liquidity, $A_i$ is the total assets held by Japanese institution $i$, and $\Delta w_i$ is the change in their weight toward domestic bonds. When you plug in the numbers for entities like the Government Pension Investment Fund (GPIF), the result is a number that can move markets on every continent.

The Fragility of the Transition

The biggest risk right now is a policy error by the Bank of Japan. If they move too fast, they trigger a global market crash as carry trades unwind overnight. If they move too slow, they risk domestic hyperinflation and a total collapse of the yen’s purchasing power.

They are walking a razor-thin line.

Regional neighbors are watching with bated breath. Central banks in Jakarta, Bangkok, and Seoul are being forced to keep their own interest rates higher for longer just to prevent their currencies from being shredded in the wake of Japan’s move. This "higher for longer" environment is a death knell for the high-growth projections that many of these nations relied on to justify their massive infrastructure spending.

Survival of the Fiscally Fit

The nations that will thrive in this new era are those that have spent the last decade building robust domestic tax bases and reducing their reliance on foreign-denominated debt. Those that used the years of cheap yen to paper over structural deficits are about to face a reckoning.

We are entering a period of "financial Darwinism" in East Asia. The financing model that powered the "Asian Tiger" miracles and the subsequent emerging market boom is being dismantled. In its place, we are seeing a fragmented, more expensive, and far more volatile system.

Investors can no longer rely on a single central bank in Tokyo to subsidize their risk. The safety net has been pulled away, and the floor is much further down than most people realize. The shift isn't just coming; it is already here, and it will redefine the economic hierarchy of the Pacific Rim for a generation.

Watch the long-term JGB yields. When they cross the 2% threshold, the real exodus of capital from the rest of Asia begins.